Here’s how much you can retire with if you put away R1,000 every month in your 20s and 30s

10X Investments has published its inaugural Retirement Reality report.

The report is the result of a comprehensive survey conducted among over 1 million South Africans to reveal the extent of the country’s private retirement fund crisis.

It takes an in-depth look at the lived financial and savings habits reality of South Africans across all demographics and indicates the savings disparity among racial groups as well as the massive divide between men and women.

According to the report, South Africans have a profound lack of understanding of what they have saved and what they need to have saved among existing clients of the retirement industry.

The poll further highlights some worrying trends across within South African demographics.

- 62% don’t have any form of retirement plan or have little understanding of their existing policy;

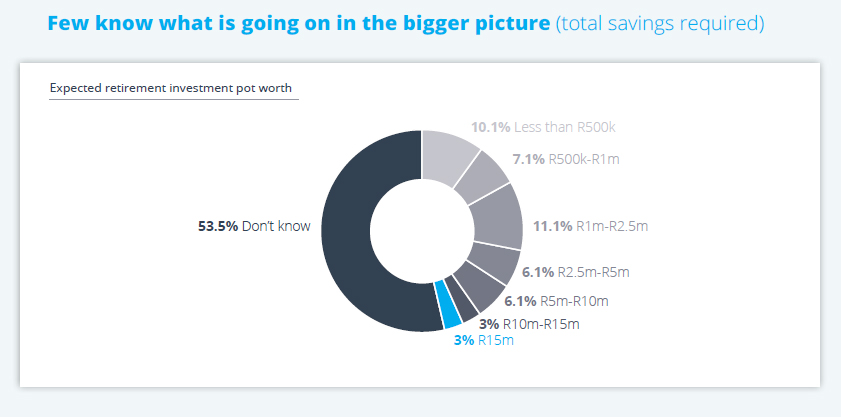

- 53% don’t know how much their pension is worth;

- 62% lack trust and confidence when it comes to investing money;

- Less than 35% of black African respondents have a pension or provident fund;

- Less than 20% of black African respondents have a retirement annuity;

- More than 40% of women across all demographics have no investments or savings in any form;

“The industry has amassed wealth at the expense of its clients, who frequently discover how poorly their retirement products have performed only when it is too late to do anything about it,” said founder and CEO of 10X Investments, Steven Nathan.

“The industry’s messaging makes strong emotive appeals. It’s high time that the facts get some airtime,” he said.

Savings goal

Fewer than 50% of the respondents were aware of how much money they could expect at retirement.

“That should not be a surprise considering how many people don’t have a retirement plan or just a vague outline,” said 10X

“This phenomenon is by no means particular to South Africa. However, considering that the onus is on fund providers to keep savers informed about their savings, there is clearly scope for the industry to do a better job in engaging, informing and educating their clients.

“While it may seem too complicated for those of us without financial knowledge, there are only a few factors which have a significant impact on determining how much money savers can expect at retirement. And, thankfully, technology makes doing the actual calculations quite simple.”

When they are starting

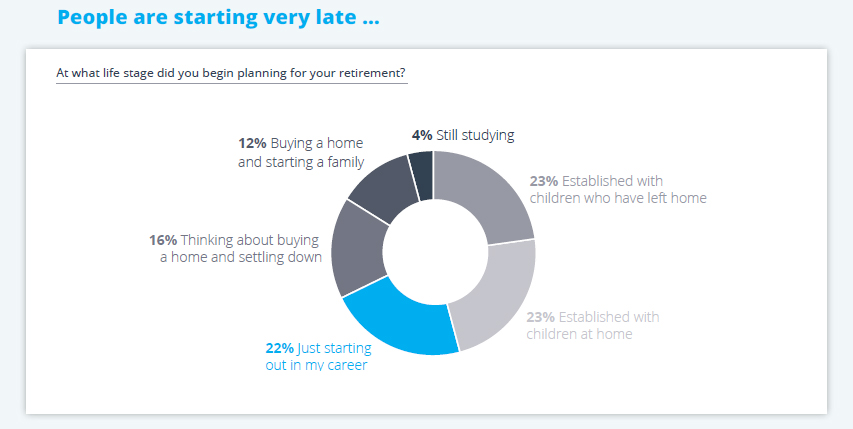

The data shows that almost half of respondents (46%) began planning for retirement only after becoming established with partners or having children, while just 22% began planning at the beginning of their careers, which is what is recommended.

“The benefit of starting to save early cannot be stressed enough,” 10X said.

“It can be very difficult to start saving for retirement when you are just starting out at work and retirement seems light-years away. But starting out early and putting a little away every month and leaving it to grow over the decades is so much more manageable than starting late and trying to catch up.”

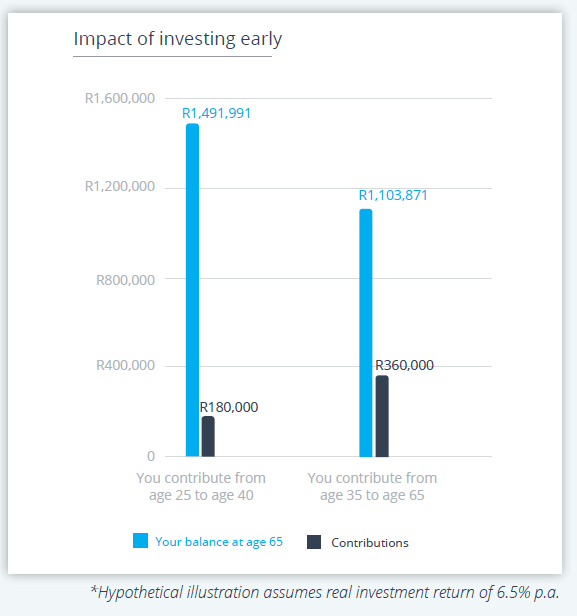

R1,000 a month

This example illustrates how powerful compounding is and the importance of starting early, 10X said.

“Imagine you start saving at age 25 and dutifully put away R12,000 a year (equivalent of R1,000/month) and then for some reason you need to stop saving at age 40.

“Your friend starts saving much later in life and saves the same R12,000 a year for the next 30 years, until you both retire. At that point in time, all else equal, you’ll have more money than your friend even though you have only contributed half the money, over half the number of years.”

Read: Have you left South Africa and need to access your retirement?