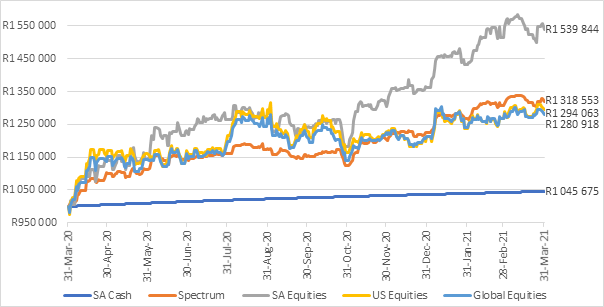

R1 million invested in these different options a year ago would be worth this much today

After the rand plummeted and blew out to more than R19 to the dollar early last year, there has been a lot of debate around taking more investments offshore and easing restrictions of offshore investing, note Yuvern Dokie, senior technical investment specialist, and John Anderson, executive, investments, products and enablement at Alexander Forbes Investments.

The analysis and discussions that follow consider the different markets and how they stack up against a balanced solution.

During the peak of the Covid-19 pandemic, both local and global markets fell drastically, and a lot of attention was given to offshore investing. In the chart below, we consider the retirement savings balance at 31 March 2021 of an individual who panicked on 1 April 2020 because of the negativity around the rand and South Africa, switching all their investments to be 100% offshore.

We compare this to what they would have earned in SA equities or in a typical balanced fund.

R1 million invested in different options on 1 April 2020 to 31 March 2021

Investing for retirement is for the long term

There has been plenty of volatility over the year, but local equities have delivered north of 50% over the year ending 31 March 2021, almost double of what the global market index gave us over the same period in rand terms. Although it is a short period, the merits of the analysis and the risk of listening to the noise and following a trend blindly rather than sticking to good long-term investment principles should be considered.

Extending the analysis to a longer period, from 1 January 2001 to 31 March 2021, the results show that 90% of members remained invested in their strategies despite the three market crashes of the Dot-com bubble and 9/11; the global financial crisis; and more recently, the market crash due to the Covid-19 pandemic.

Overall, default strategies adopted by retirement funds have fared well to ensure that members remain appropriately invested for the long run.

Investing for retirement is for the long term, so do not get caught up in the short-term noise. Base decisions on sound investment principles that have been tried and tested and stay level-headed through investment markets.

Markets move in cycles

When using rolling 5-year returns, which tie into the time horizon used for a global balanced portfolio, the returns have shown interesting results:

A typical balanced fund met an inflation + 5% real return target 53% of the time, with no rolling 5-year periods showing negative returns.

In contrast, investing 100% offshore would have resulted in meeting the inflation + 5% real return target only 40% of the time, with 13 rolling 5-year periods showing negative returns.

Markets move in cycles and we do not know which cycle will be next. We do know, however, that we need sensible principles, and we need to be positioned for different types of outcomes in a balanced approach. It is imperative to marry risk and the expected return.

Regulation has adapted to the change in environment

Offshore limits have increased over time to allow for more allocation to offshore. The changes over time have shown evolving regulation and relaxing of regulations to accommodate different investment environments.

Looking at investment principles for pensions, South Africa compares reasonably well with other countries based on where pension funds typically invest. There is a local bias in any country’s pension fund allocations as the liabilities are in the home currency.

Many listed companies on the JSE have offshore exposure through offshore earnings which needs to be considered when identifying the “true” allocation to offshore.

Balanced funds show an attractive risk-return profile as a result of diversification

Alexander Forbes analysis shows our best investment view of what a post- and pre-retirement solution should look like to deliver on their long-term inflation objective.

The analysis shows that the optimal asset allocation uses a blend of offshore and local asset allocations, with the “sweet spot” of strategic offshore allocation being between 25% and 27.5% at present for accumulation portfolios, which is within the regulation limits.

In addition, Alexander Forbes analysis shows that for pensioners the optimal asset allocation depends on the individual’s preference for an income or legacy, as well as the level of drawdown of the individual.

- By John Anderson, executive, investments, products and enablement at Alexander Forbes Investments