Tax-free savings in South Africa and how to get the best returns

In 2015, National Treasury introduced tax-free savings accounts (TFSAs) to improve the overall savings rate of South African citizens. It’s not often you get a gift from government, especially in the form of a tax-saving, so it is best to make the most of it, says Roné Swanepoel, business development manager, Morningstar Investment Management South Africa.

With any investment, there are taxes to be paid. To maximise your tax-saving when investing, you need to know what taxes you are paying and how this tax might impact your investment. This will enable you to structure your investment in the most tax-efficient manner, said Roné Swanepoel.

What taxes are payable for which investments?

Different investments will attract different taxes. Investors are also given some reprieve in the form of certain exclusions with regards to the different taxes that are payable.

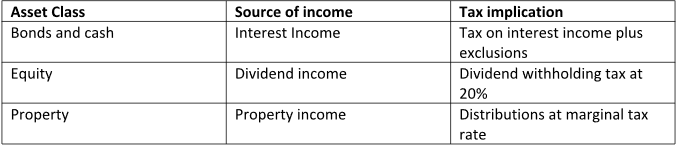

- Interest tax – Bonds and cash in unit trust investments will incur interest tax. Interest earned from a South African source, earned by any natural person is exempt per annum, up to an amount of R23,800 for individuals younger than 65 and R34,500 for individuals older than 65.

- Dividend income – Dividends received by individuals from South African companies are generally exempt from income tax, but dividends tax, at a rate of 20%, is withheld by the entities paying the dividends to the individuals. This means that 20% of your dividends will be held back before the balance is paid out to you or reinvested.

- Property investments – Real Estate Investment Trusts, also referred to as REIT’s, have a more complex structure. In essence, investors pay income tax on the distributions they receive at their marginal tax rate.

- Capital Gains Tax (CGT) – Lastly CGT comes into play when an investor decides to sell part of or their entire investment. If the price of the investment has increased since the time you invested, you will have to pay tax on this gain/profit. A portion of your capital gain gets added to your other income for that year and you are taxed at your marginal tax rate (your combined earnings for that tax year are taxed). The CGT rate can range from 7.2% to 18% depending on the tax bracket you fall in. Only 40% of a capital gain is included and there is also an annual exclusion of R40,000.

The basics of a tax-free savings account

A TFSA allows an individual to invest in various asset classes without having to pay income tax, dividends tax or capital gains tax on the returns from these investments. These accounts can be opened with various banks, asset managers, life insurers and stockbrokers, noted Swanepoel.

The annual limit for individual investors in the product is currently R36,000 and the lifetime limit per investor is R500,000. Contributions must not exceed the annual individual limit of R36,000, as any contributions over and above this amount are taxed at a rate of 40%.

A TFSA is a long-term investment

The term “savings account” is rather unfortunate, given the fact that most individuals would associate this with something that is short-term in nature and easily accessible to fund any unexpected expenses. At Morningstar, we view these investments as long-term savings vehicles, with returns maximised through capital and income growth and compounding over extended periods of time.

There are some important points to keep in mind when investing in a TFSA which Swanepoel has set out below.

Over or under contribution:

An example of an under-contribution will be if “Investor A” only contributes R30,000 to his/her TFSA on the 2020 tax year. The remaining R6,000 that is available to Investor A will not be rolled over to the next tax year and the benefit is therefore forfeited.

An example of an over-contribution is where “Investor A” contributes R40,000 to his/her TFSA in the 2020 tax year. This means, “Investor A” contributed R4,000 above the annual limit of R36,000 and will be subject to a tax rate of 40% on the over-contribution.

Can an individual have more than one TFSA?

Any person (including minor children) can have more than one tax-free investment, however, the annual limitation is an aggregation per year of assessment. For example, in one tax year, you can invest R11,000 in fund A, R11,000 in Fund B and R14,000 Fund C.

Withdrawals during the investment term

It is possible to withdraw funds during the investment term but keep in mind that the penalty for withdrawing your funds is that any funds withdrawn cannot be replaced and permanently reduce your TFSA limit, said Swanepoel.

“Another benefit of these accounts is that it is not subject to any regulatory limits in terms of where the money can be invested. A TFSA, therefore, allows an individual to diversify away from South African specific risks through a highly tax-efficient product, without restrictions in how the money is invested.”

She said that the question that often get asked is – if I can invest in any asset class, what’s the ideal asset allocation for a TFSA?

“We recommend that investors think of a TFSA as a minimum of a 15-year investment (i.e. using your annual allowance every year but not exceeding the R500,000 lifetime limit).

“While risk tolerance is likely to be different for each investor and based on their personal circumstances, the nature of the product, however, means that investors will gain the most benefit from significant allocations to growth assets. This would be mainly based on the long- term outperformance of these asset classes against more conservative allocations, such as fixed income and cash.”

Swanepoel said there are clear benefits of using a TFSA within your retirement and savings planning to eliminate the taxes that you would have been subject to using other investment vehicles.