Double blow for pension fund members in South Africa

South Africans with retirement funds have been warned about the long-term consequences of withdrawing from their two-pot funds, especially amid current market volatility.

Retirement funds were subject to new legislation in 2024, when the two-pot system came into effect, allowing limited access to funds while ensuring that the majority of funds remain untouched.

The two pots include a savings pot, into which one-third of retirement savings are placed, and a retirement pot that holds the remaining two-thirds.

Ninety One’s Jaco van Tonder said that the start of the new tax year has triggered a fresh wave of withdrawals from the savings pot under South Africa’s two-pot retirement system.

Pension fund administrators have reported that requests began almost immediately after the new tax year opened this month.

Van Tonder said that this reflects two things: retirement fund members are under real financial pressure, and the withdrawals appear to be concentrated among repeat users of the system.

“While the behavioural pattern is understandable, the timing of this year’s withdrawals could hardly be worse,” he said.

“Towards the end of February, the market backdrop looked relatively constructive. South Africa’s Budget was broadly well-received, and sentiment towards local assets had improved.”

However, the conflict in the Middle East following America and Israel’s attacks on Iran and the Persian nation’s retaliatory strikes has led to a sharp spike in oil prices and risk-off sentiment.

This has led many portfolios to experience meaningful declines over the period. This has two major problems for members.

They are not only reducing their retirement savings, but are doing so in a period when markets have already fallen. This means that the losses are locked in for the investor.

“The mathematics of investing makes this particularly damaging. If a portfolio loses 50%, it doesn’t require a 50% gain to recover. It requires a 100% gain.”

“By withdrawing after a drawdown, investors reduce the capital base and increase the return required to rebuild their retirement savings.”

Van Tonder said this pattern reflects a classic behavioural finance mistake, in which investors feel they must react to volatility.

This desire to do something can lead to long-term wealth losses. Withdrawing from equity-based investments after a market decline is one of the most common and costly examples.

Long-term pain

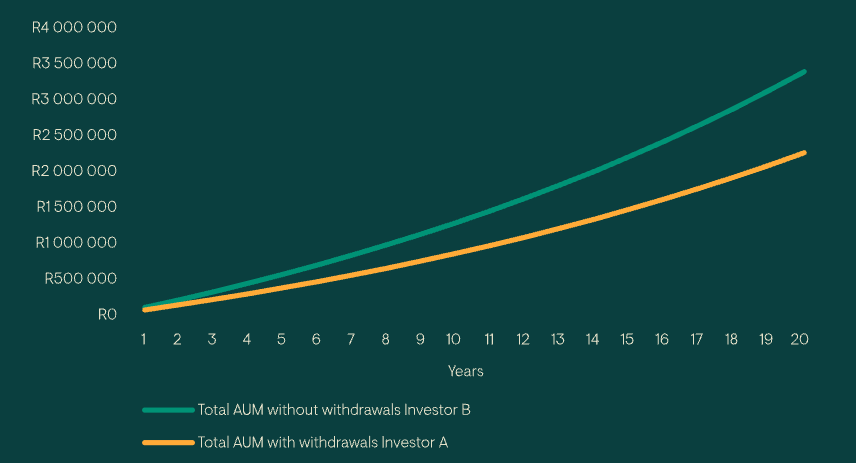

Even when market volatility is ignored, repeated withdrawals from the savings pot can carry a massive long-term cost.

All withdrawals reduce the capital that would otherwise compound over decades. Withdrawing from the savings pot consistently before retirement can reduce an investor’s eventual nest egg by around a third.

“That is the real long-term risk embedded in the system. The two-pot structure was designed to provide flexibility during financial hardship, but frequent use undermines retirement security,” said Van Tonder.

“If two-pot withdrawals become a regular habit rather than an emergency measure, the gap between what people save and what they need for retirement will widen even further.”

He added that periods of market turbulence are uncomfortable, but they are a normal part of long-term investing.

Markets have experienced many short-term shocks for decades, such as oil price spikes, inflation scares and recessions. Over time, they recover and move higher.

“The key principle for long-term investors remains unchanged: stay invested, avoid locking in losses, and allow time and compounding to do their work.”

“For retirement savers considering a two-pot withdrawal right now, the most important question is simple: Is this truly necessary?”

Timing the market is extremely difficult when investing. However, withdrawing during market stress is often the exact opposite of what one should do to build wealth.