Allianz Trade South Africa Country Risk Report

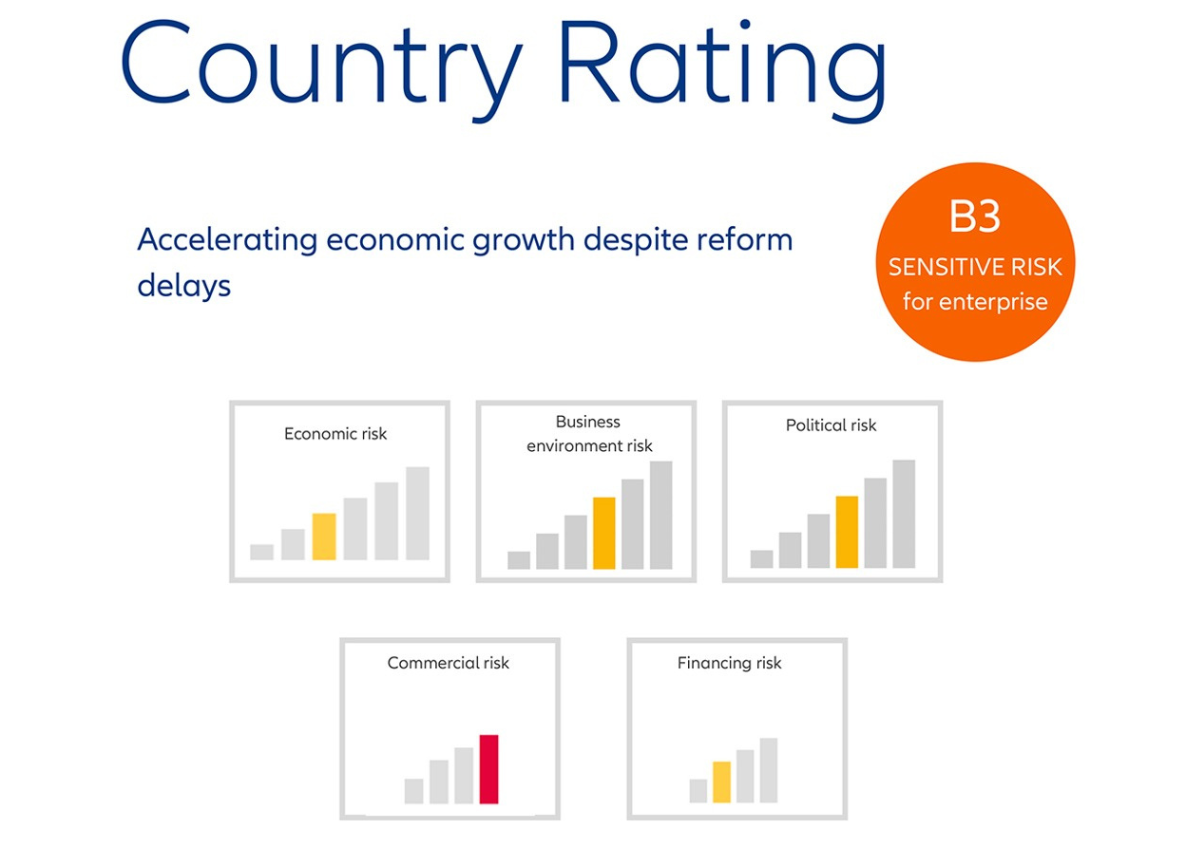

South Africa: Accelerating economic growth despite reform delays

Economic growth in South Africa is forecasted to gain further momentum in 2025, doubling to +1.5% after a sluggish +0.7% in 2024.

Following the general election, consumer and business confidence has risen, driven by increased trust in the Government of National Unity (GNU) and its potential reforms. Yet, Allianz Trade believes the most tangible improvement to economic activity has been the end of electricity loadshedding since March 2024. However, the mining sector, which accounts for a significant portion of exports, remains weak, along with the agriculture sector, which also saw a drop in output from the previous year.

Economic activity growth in 2025 will be supported by new reforms and an improved electricity supply. The coalition between the African National Congress (ANC) and the Democratic Alliance (DA) has brought in a more business-friendly government and introduced a new layer of checks and balances within the South African government.

As the continent’s most diversified economy, South Africa has historically been hindered by weak infrastructure, as evidenced by the underperformance of the mining sector. Throughout 2023 and 2024, mining activities lagged during a period when other mining powerhouses like Australia and Brazil thrived. Poor train and port connectivity hampered exports and overall output. Similarly, the electricity sector has significantly impacted economic activity due to frequent blackouts and unreliable supply.

Momentum building in the South African economy

However, improvements in electricity supply during the first half of 2024 have led to increased output in manufacturing and retail sales. Despite these improvements, the country’s electricity issues are deep-rooted and unlikely to be fully resolved in the short term.

The new infrastructure minister in the GNU has pledged to boost investment to address supply-side challenges, including ports, roads, the power grid and water infrastructure, which could enhance both economic output and productivity. Yet, reforms could be hindered by poor policymaking and political interests.

Inflation is forecasted to continue gradually declining to 3.9% in 2025. The central bank is currently adopting a dovish stance. In this context, we anticipate a declining trend in insolvencies and positive economic performance in the latter half of the year.

External vulnerabilities have diminished, with foreign debt to GDP below 20% since 2021, and expected to slightly increase in 2025 to 19.8%. Due to a considerable short-term absorption of revenues to repay interest on debt, South Africa ranked in the worst quintile in our public debt sustainability risk assessment as of end-2024. The overall balance is expected to slightly increase in 2025 to -6.3%, after an estimated -6.2% in 2024.

Government revenues saw a decline during 2024 due to the decrease of energy-generation imports, including solar panels and crude oil, which reduced tax duties collected. As a result, fiscal consolidation disappointed during 2024, with a deficit around 5% by end-2024, and it is expected to improve only marginally in 2025.

The 2025 budget should provide better guidance on the deficit path.

The level of government debt remained elevated at 75% of GDP in 2024 and is forecasted at 77% in 2025; the ratio has significantly increased from the 2011-19 average of 45%.

Interest payments are part of the price of the favourable debt structure, which is primarily denominated in local currency and has a lengthy amortization profile on average (12 years), and that provides some room to manoeuvre in the country’s debt profile.

After a year of appreciation, the South African rand reversed its course in late 2024, offsetting the gains and finishing the year at 18.77USD/ZAR.

International reserves followed a similar path: With an increase above USD61bn, the year closed just above USD60bn, around six months of imports, double the level commonly seen as critical for emerging markets.

A disappointing fiscal outlook

Since taking office, President Cyril Ramaphosa has faced challenges in implementing effective reforms.

Inflation, demographic pressures and the highest inequality levels in the world have made South Africa’s social contract increasingly unstable, particularly since the Covid-19 pandemic.

While the immediate health crisis has passed, its social consequences remain significant.

The unemployment rate, currently above 33%, has been gradually rising and is nearing the historical peak of 35% reached during the pandemic.

Similarly, school dropout rates and the number of children receiving no schooling have increased after initially declining post-pandemic.

Commercial opportunities ahead amidst slow reforms

Despite South Africa leading in education spending among emerging markets, the quality of education remains a concern, contributing to persistently low productivity.

The ruling ANC party’s ability to implement reforms will be crucial for the country’s success.

Additionally, its capability to transition from a party with an absolute majority to a senior partner in a coalition with diverse interests will be key to enhancing the predictability and effectiveness of government actions.

South Africa’s external sector holds significant potential for delivering outstanding results but it also faces many challenges.

As a top exporter of highly valued minerals to Asia and Europe, improving South Africa’s infrastructure could increase capacity and profitability.

In addition, as a relevant exporter of cars to developed markets, mainly Germany – thanks to the numerous factories of German auto manufacturers – South Africa enjoys important skilled labour that could be expanded to new auto power houses such as China.

However, it also faces the systemic troubles of Germany’s industry.

Finally, South Africa’s value chains are well integrated into the rest of the African continent, with the newly agreed Africa-wide trade agreement, South Africa’s role in the region could significantly increase.

The geopolitical context in the Middle East has presented South Africa with an opportunity to become a focal point for global trade as traffic through the Suez Canal has been disrupted.

The Cape of Good Hope has emerged as the primary maritime connection between Europe and Asia, leading to a +328% increase in containership arrivals at South African ports since December 2023.

This surge in port traffic has also boosted port revenues. Implementing trade facilitation measures, such as improving port operations and cargo handling, could transform South Africa’s ports into major logistic hubs connecting Asia, Europe and Latin America.

Download Allianz Trade’s eBook about growing your business with credit insurance.

View a summary of the South African economy’s trade structure according to Allianz Trade, below.

Allianz Trade – Make decisions with confidence

The Allianz Trade South Africa Country Risk Report forms part of Allianz Trade’s global analysis of country risk.

By working with Allianz Trade and using its analysis, you can plan and manage your international trade strategy.

This allows you to make important international trade decisions for your business with confidence.

For a basic summary of global risk, view the image below, and click here to get a free quote on trade credit insurance.