The retirement mistake that can cost you R21 million

Allan Gray has highlighted the importance of saving for retirement as early as possible by illustrating that saving just 10 years later can cost you almost half (R21 million) of your retirement savings.

Institutional Clients manager at Allan Gray, Nshalati Hlungwane, said that many South Africans dream of a secure and comfortable retirement, but many fall short.

According to Hlungwane, this shortfall is often not due to poor intentions but to delayed action, inconsistent contributions, financial pressures, and the sheer complexity of retirement decisions.

“Thinking of retirement as a journey with specific stages can be a helpful way to overcome many of these obstacles,” said Hlungwane.

Referencing retirement expert Don Ezra, who spoke at Allan Gray’s “Through the Noise” retirement benefits conference, Hlungwane outlined a three-stage approach that can transform investors’ preparation for their later years.

The first stage is actually getting started. “Time is crucial in retirement investing. The earlier you start, the better the outcome,” Hlungwane explained.

“While it may feel like there’s plenty of time early in your career, starting sooner lets you benefit more from compound interest.”

The consequences of delaying this first step can be staggering. Hlungwane provided an example that illustrates the cost of hesitation.

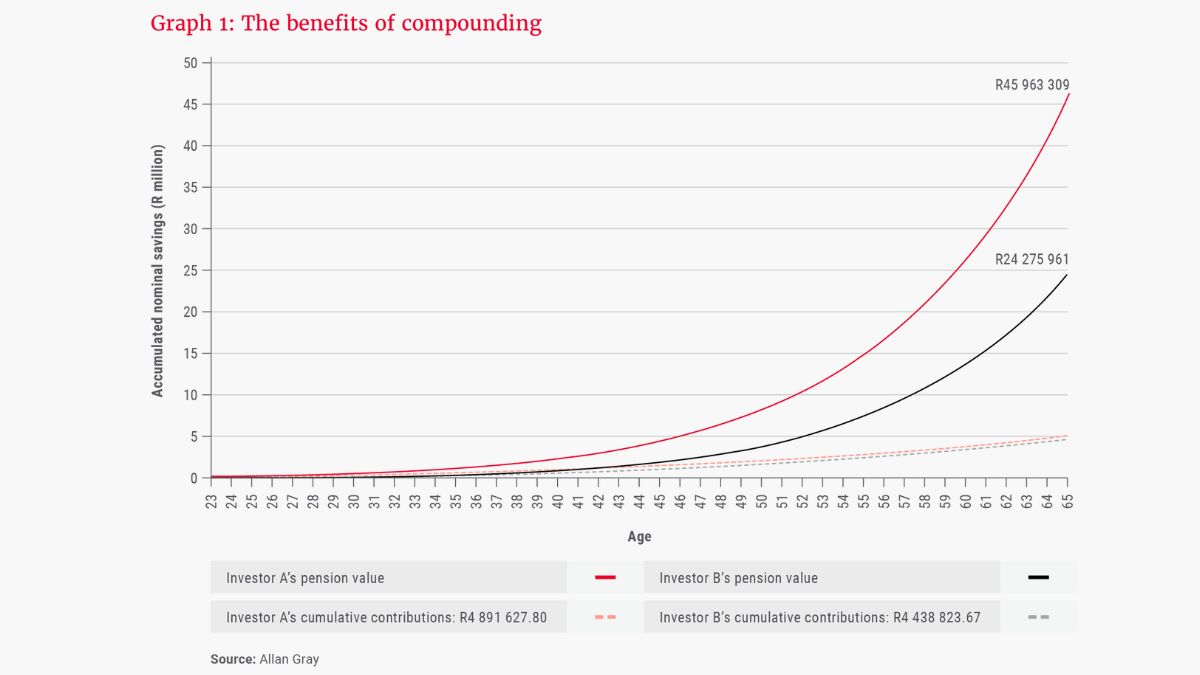

Consider two investors with identical earnings and contribution rates. Investor A begins saving 15% of a R20,000 monthly salary at age 23 and increases contributions annually with inflation.

Investor B delays saving for 10 years. Assuming an annual investment return of 11%, by retirement age, Investor A will have R45.96 million, a full R21 million more than Investor B, who accumulates just R24.28 million.

“Most of this difference comes from compound growth, earning returns today on returns earned yesterday,” said Hlungwane.

“It’s an important reminder that the earlier you start, the less you invest to achieve the same outcome.”Hlungwane also advised that investors shouldn’t shy away from risk in these early years.

“A higher allocation to volatile assets like equities early on can boost long-term returns, but investors must be prepared for short-term ups and downs,” she said.

“Market fluctuations typically smooth out over time, and losses only become real if you disinvest out of fear.”

The infograph below illustrates the cost of delaying saving for retirement by just 10 years.

Calculate what you want at retirement and ramp up contributions

Hlungwane explained that the second stage of the journey, typically from your early 40s to around five years before retirement, is about accelerating your efforts.

This phase often coincides with career stability and peak earning years, which creates an opportunity to rectify earlier gaps.

“As we mature in our careers and our salaries rise, we typically enter the peak of our accumulation phase,” said Hlungwane.

“This presents an opportunity to make up for lost time by rectifying any mistakes we made or accounting for any disruptions to our contributions in the first phase of our retirement planning.”

This is the time to ramp up contributions, both through your employer’s retirement fund and your own savings.

Hlungwane also suggested adopting an “income mindset”, thinking about how your accumulated savings will convert into a sustainable monthly income in retirement.

“It helps gauge if you’re on track – and gives you time to adjust your plan, if needed. A financial adviser or online retirement calculator can assist with these projections.”

In the final stage, the five years before retirement, the focus shifts to preparing emotionally, practically, and financially for the transition.

“These years are key to reassessing your goals, envisioning how you’ll spend your free time, and evaluating your readiness,” said Hlungwane.

“Some may delay retirement or explore new income streams; others may pursue passion projects or give back.”

However, Hlungwane warned of three key risks at this stage: capital loss, inflation eroding returns, and outliving your savings.

She recommended working with an independent adviser to develop an appropriate drawdown strategy that balances longevity, returns, and safety.