The dire state of South Africa’s state-run companies

Union Solidarity’s Research Institute has published a report on the state of state-owned companies, showing how government guarantees and bailouts effectively entrench poor performance at state-run firms.

According to Solidarity, state companies should, in theory, work in the interests of the country; however, with access to billions in funding and guarantees, there is little to incentivise efficient business practices, and little to no accountability for management teams that fail to meet targets.

“State-owned enterprises are often viewed as a trade-off between the interests of the state and commercial considerations,” Solidarity said. “These entities, therefore, are required to maintain a balance between the public interest and financial stability.”

“Put differently, their activities should not only be advantageous to society but also economically justifiable. The problem, however, is that often these companies do not succeed in achieving either of these objectives.”

According to the Presidential State Institutionas Revision Committee, there are at least 715 state institutions with access to huge cash and funding channels through government.

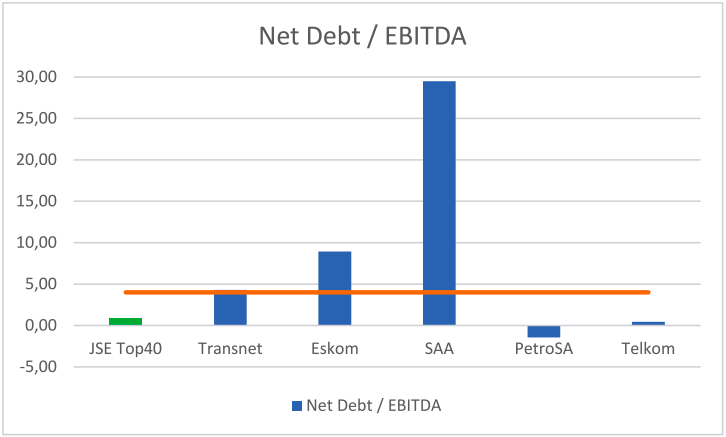

Solidarity’s report focused on five of the biggest SOEs, including Eskom, Transnet, PetroSA, Telkom and SAA, and delved into the their finances – looking at their working capital ratio, ned debt against ebitda and weighted their financial soundness against the JSE top 40.

Here, the working capital ratio for the JSE top 40 was at 1.53, while the net debt to ebitda is at 0.92.

This is how the SOEs compared:

| Company | Working capital ratio | Net debt / Ebitda |

|---|---|---|

| PetroSA (2015) | 2.31 | -1.43 |

| Telkom (2017) | 1.06 | 0.43 |

| JSE Top 40 | 1.53 | 0.92 |

| Transnet (2017) | 0.45 | 4.30 |

| Eskom (2017) | 1.00 | 8.92 |

| SAA (2016) | 0.54 | 29.48 |

Of the state companies analysed, only PetroSA showed a working capital ratio that was higher than the JSE Top 40 standard, pointing to state companies not managing their finances well and are dealing with debt irresponsibly.

Because the government is always sitting in the wings, ready to bail SOEs out, there is little incentive for the companies to function on their own terms, repaying debts from their own earnings, Solidarity said.

With the debt against ebitda ratio, the picture gets worse – where only PetroSA and Telkom keep their ratio below 4.0, which is considered to be dangerous territory. In PetroSA’s case, this is only an illusion of security created by huge cash reserves, Solidarity said.

In Telkom’s case – compared to the other SOEs analysed, the company is doing quite well. However, Solidarity notes that the difference here is that government is only a shareholder in the company, and that the partial privatisation keeps it competitive.

“It is painfully clear that these institutions are not aimed at financially autonomous functioning,” the union said. “In a normal market environment, managers who caused their companies to end up in these situations would have been removed by furious shareholders long before it could happen.”

SOEs are not isolated from the economy and compete with private businesses, and they are given artificial buying power, Solidarity said. Ultimately this entrenches poor management and increased input costs, to the detriment of the economy and taxpayers as a whole.

“When major projects that are economically or politically inappropriate – such as Sanral’s e-toll project – are subsidised by inefficient SOEs using tax money and state guarantees and kept alive artificially, such projects become a millstone around the neck of the taxpayer,” the group said.

The union said that South Africa’s state companies should be privatised as far as possible, so that they can be run by business people, rather than bureaucrats.

“South African taxpayers simply cannot continue funding the cadre merry-go-round,” it said.

You can view the full report here.

Read: South Africa’s government wage dilemma: pay up, or face more strikes