The majority of South Africans are now working into retirement

The majority of South Africans can no longer afford to retire, relying heavily on income from a salary because their pension income is insufficient to support them.

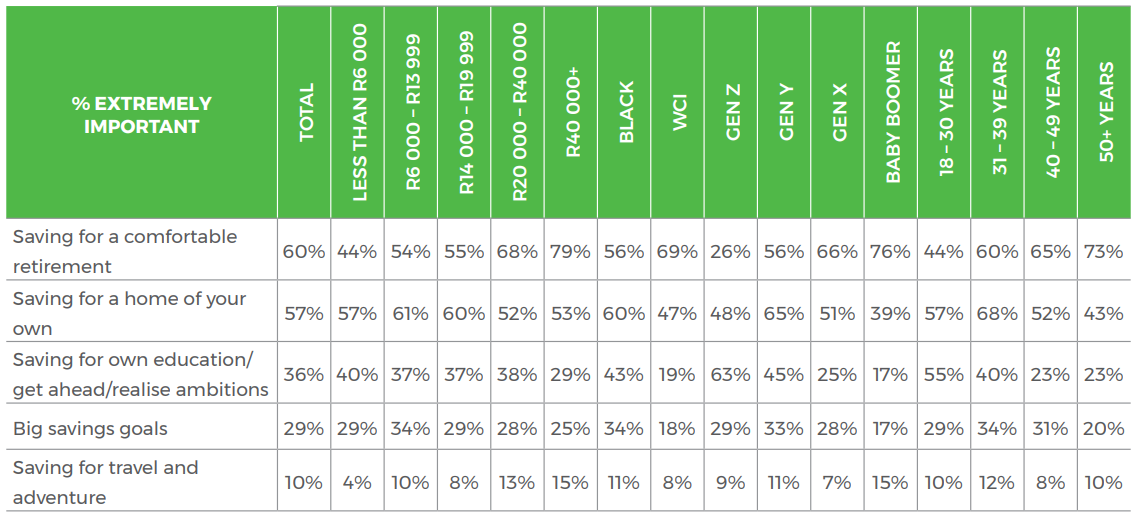

This is one of the major findings of the 2019 Old Mutual Savings and Investment Monitor which tracks shifts in the financial attitudes and behaviour of South Africa’s working metropolitan population.

Criteria for inclusion of retirees into the study – which was released Monday (15 July) in Sandton – was that they receive a monthly income in some form of at least R15,000.

“Including this demographic into our study reveals the impact that many households suffer because they are financially underprepared for their retirement,” said Lynette Nicholson, research manager at Old Mutual.

“While one’s sunset years are supposed to be a time to kick back and enjoy the pleasures that life has to offer, this does not appear to be the case for many of those we surveyed. What our study shows is that as many as 92% continue to work because they are dependent on additional income to make ends meet.”

The monthly contribution from a pension for nearly 80% of people makes up only 27% of their income, with other investments or savings contributing only 7%.

Tightening belts

The survey results show that half of retirees are working for an employer, 36% have started a business post-retirement, while 13% have continued to be self-employed or taken up a position as a consultant.

An important context to the results is that 53% of retirees are still supporting dependent children and or grandchildren, of which 41% are supporting dependents under the age of 12, Nicholson said.

A further 9% of respondents are supporting parents or even grandparents, with those most under pressure (26%) being classified as the Sandwich Generation because they are squeezed between supporting older as well as younger generations.

To combat these issues, Old Mutual’s research shows that retirees are actively cutting down their expenses in order to cope financially.

Those polled in the survey are tightening their belts by spending less on clothing and shoes (45%), holiday and travel (41%), eating out and entertainment (39%), electricity and water (38%), entertaining at home (37%) and cell phone air time (36%).

Similar to the results from the non-retiree market, nearly two-thirds of their income is directed toward living expenses, with 14% going to savings. Understandably, the proportion committed to insurance and medical (10%) is double that of non-retirees.

“The lack of preparedness for retirement could be measured to some degree by only 4% of respondents leaving their pension or provident fund lump sum intact and opting to receive a monthly pension,” Nicholson said.

“This is the ideal situation as these pensioners should be better equipped over the long term to survive financially.”

“The 21% of respondents who took the entirety of their pension in a lump sum are potentially worst prepared for the future. And the 75% who took a portion as a lump sum and the rest as a monthly pension made a far wiser decision.”

She adds that households that manage to reduce their indebtedness in the later stages of their life are best prepared to see through their retirement in relative comfort.

“Not only is it prudent to reduce monthly expenses when in retirement, but severe financial stress can be reduced by having a long-term savings plan and outlook,”she said.