South Africa faces another downgrade decision on Friday

Moody’s Investor Services is scheduled to release its credit rating review for South Africa on Friday (1 April), the first of three rating decisions expected in the coming weeks, says Nedbank.

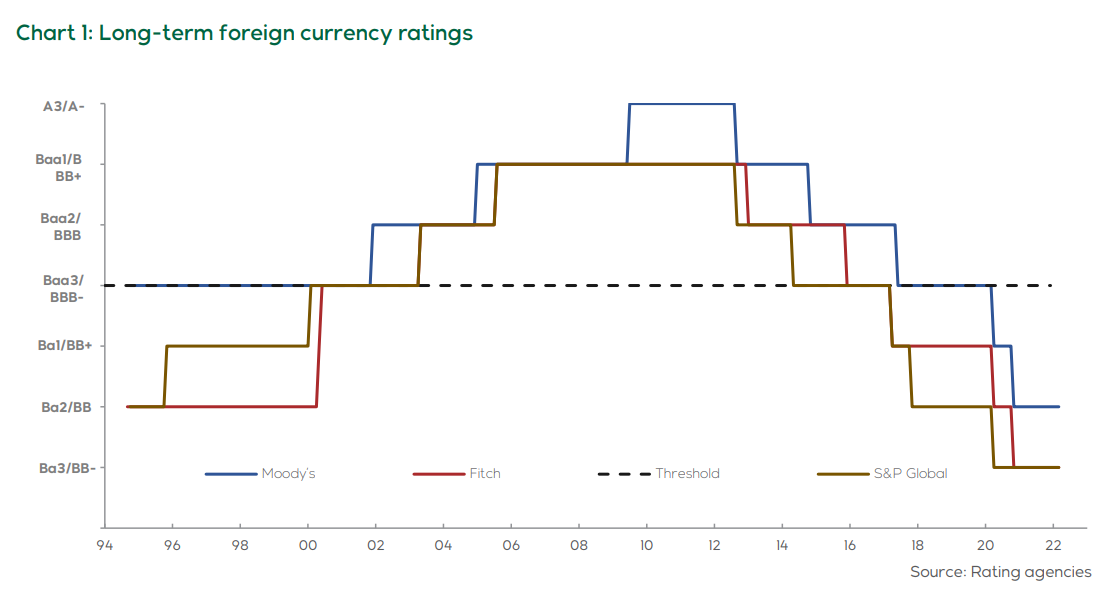

S&P Global Ratings is scheduled to publish its ratings review on 20 May, while Fitch Ratings is expected to publish its review around the same time, the bank said in a research note on Friday.

The agencies assess several factors that currently point to the current ratings being maintained, the bank said.

“The National Treasury continues to demonstrate its commitment to stabilise public finances, which deteriorated dramatically over the past decade. However, much of its success will depend on the growth trajectory and the government’s ability to exercise expenditure restraint.

“The government will need to limit growth in non-investment, albeit critical functions, while accelerating and improving the efficiency of spending on investment projects. This, coupled with more policies to unlock the growth bottlenecks in the network industries, will boost the growth rate and the economy’s capacity to create jobs.”

Nedbank added that the government has little room to manoeuvre on debt service costs, and the pace of fiscal consolidation will depend on containing the public sector wage bill and boosting economic growth.

“The revised fiscal ratios will help avoid further credit rating downgrades instead of improving the chances of an upgrade in the foreseeable future. Even with the lower figures, South Africa’s ratios remain well above the medians of BB-rated sovereigns.

“As such, we expect Moody’s and Fitch Ratings to affirm their credit ratings and maintain a stable outlook, and S&P Global Ratings to affirm its rating but revise the outlook to stable from negative.”

Nedbank said the three rating agencies are likely to focus on the following issues when issuing their ratings:

- Macroeconomic reforms – Recently announced policies aimed at boosting investment and economic growth are encouraging, but the pace of reform is still slow.

- Economic growth – The local economy was buoyed by the favourable global environment in 2021, benefitting from global demand and high commodity prices. However, domestic demand growth was relatively subdued, with several once-off and persistent factors disrupting its momentum.

- The fiscal position – The government remains committed to reducing the budget deficit and containing the growth in the public debt stock. Stronger economic growth and higher-than-previously projected revenue collections help to improve the fiscal ratios over the Medium-Term Expenditure Framework period (MTEF − 2022/23 to 2024/25).

- The budget deficit – The deficit will narrow slowly and stay well above the BB median of 2.8%1. Financing the deficit will not be a significant challenge due to the deep local capital markets and the sovereign’s access to global capital markets. However, the ratio of local currency government bonds held by international investors has dropped sharply to below 25%, which indicates a narrower investor base.

- Public sector wage bill – The 2022 Budget set the growth of the wage bill at 1.8% a year between 2022/2023 and 2024/25.

- Debt service costs – The elevated public debt stock will increase interest payments by 12.2% to R310.8 billion in 2022/23.

- Social grants – The government has extended the Social Relief for Distress (SRD) grant to March 2023, costing R44.4 billion in 2022/23.

- Public debt – The narrower budget deficit helps contain the debt-to-GDP ratio’s growth over the MTEF. The National Treasury projects the ratio to ease to 69.5% in 2021/2022 before rising steadily to peak at 75.1% in 2024/25 and to ease to 70.2% in 2029/30.